Most Pakistani ecommerce operators believe cash-on-delivery is an immovable consumer behavior — that Pakistani buyers simply will not pay before receiving their order. Data from the Asian Development Bank, reported by BeingGuru, tells a different story: 87% of ecommerce payments in FY24 were initiated through bank accounts or digital wallets, even as 93.7% of orders still arrived COD. The gap between payment initiation and completion is not a technology problem. It is a trust architecture problem at checkout.

Why does the “Pakistan only pays cash” narrative persist?

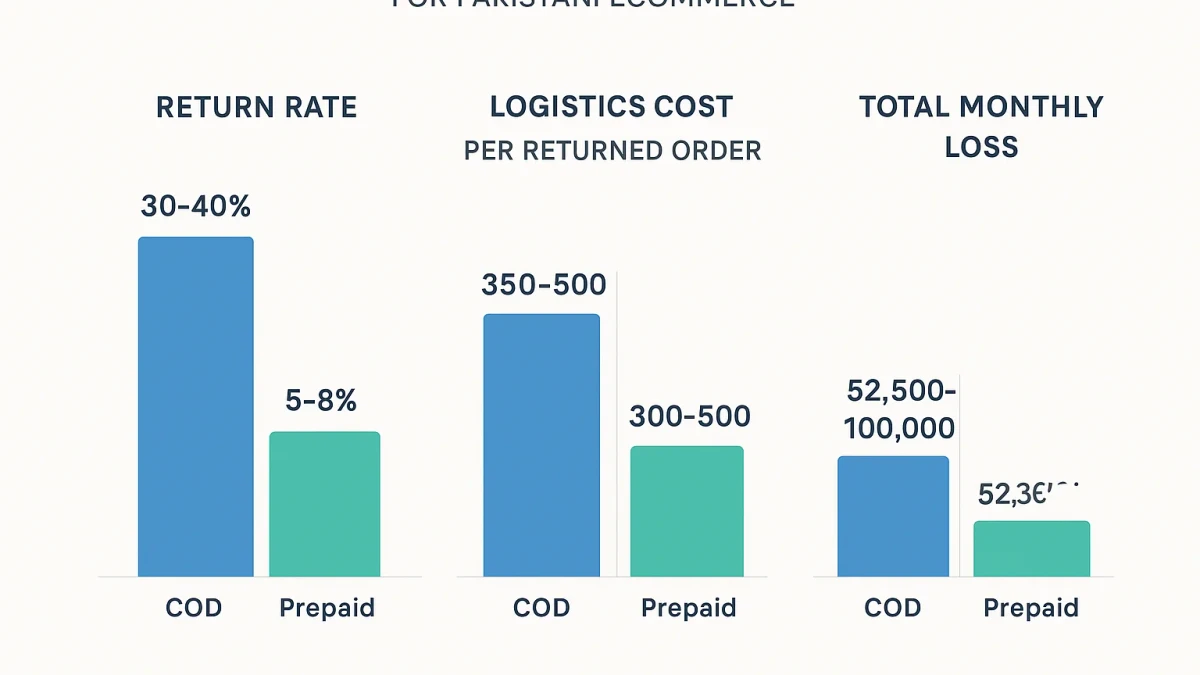

The narrative survives because the return rate on COD orders masks the real cost structure. A Karachi fashion store shipping 500 COD orders per month at an average order value of PKR 3,500 faces a 30-40% return-to-origin rate, according to ecommerce marketing analysis from ATNRCO. Each returned order costs PKR 350-500 in logistics alone — the courier charges for the outbound trip regardless of whether the buyer accepts the package. Multiply that across 150-200 returned orders monthly, and the store burns PKR 52,500 to PKR 100,000 on shipments that never convert to revenue. Prepaid orders, by contrast, carry a return rate below 8%.

What actually drives this is the absence of trust signals at the moment of payment commitment. Pakistani consumers are not opposed to paying upfront; 89% of retail transactions in Q3 FY25 were already digital, processed through JazzCash, Easypaisa, and bank transfers. The average Pakistani smartphone user completes 5-7 digital transactions per week — bill payments, mobile top-ups, ride-hailing, food delivery. The reluctance is specific to ecommerce checkout, where the buyer cannot verify product quality, sizing, or delivery timeline before committing funds.

The pattern repeats across Pakistani ecommerce. Stores invest in Meta ads, influencer partnerships, and product photography, then present a checkout page with no buyer protection messaging, no delivery timeline guarantee, and no visible refund process. The buyer defaults to COD not because they prefer cash, but because the store has not earned enough confidence for a prepaid commitment.

How much does cash-on-delivery actually cost a Pakistani ecommerce store?

The cost of COD extends far beyond return logistics. According to PACRA’s media sector research for FY24, digital advertising revenue in Pakistan reached PKR 35.8 billion, accounting for 31.2% of total ad spend. Pakistani ecommerce stores pour significant budget into Meta and Google ads to acquire traffic, but when 71.5% of carts are abandoned — as documented by ATNRCO’s ecommerce analysis — and most remaining orders arrive COD, the effective customer acquisition cost doubles or triples compared to a prepaid model.

Consider the full cost stack. A Lahore beauty brand spending PKR 200,000 monthly on Meta ads generates roughly 2,000 clicks at an average CPC of PKR 100. Of those, perhaps 120 add to cart and 35 complete checkout. If 30 of those 35 choose COD and 10 return the product, the brand has spent PKR 200,000 to acquire 25 paying customers — a customer acquisition cost of PKR 8,000. The same store with a prepaid checkout optimization, reducing returns to 2 out of 35, acquires 33 paying customers at a CAC of PKR 6,060. That difference compounds over 12 months into hundreds of thousands of rupees in recovered margin.

Cash handling fees add another layer. Couriers charge 2-3% of order value for COD collection, and the remittance cycle stretches 7-14 days. A store doing PKR 2 million monthly in COD revenue pays PKR 40,000-60,000 in collection fees and waits up to two weeks for cash flow. Prepaid orders eliminate both the collection fee and the remittance delay, improving working capital immediately.

The hidden cost compounds across the entire operation. COD-heavy stores require larger warehouse space to hold returned inventory. They need more customer service staff to handle return-related complaints and reshipment logistics. They face higher chargeback risk when COD orders are processed through payment gateways for partial prepayments. Every one of these operational costs traces back to a single root cause: the buyer did not commit payment before the product left the warehouse.

Is the digital payments infrastructure already in place?

Book a free strategy call - we'll audit your current setup and identify the highest-impact fixes.

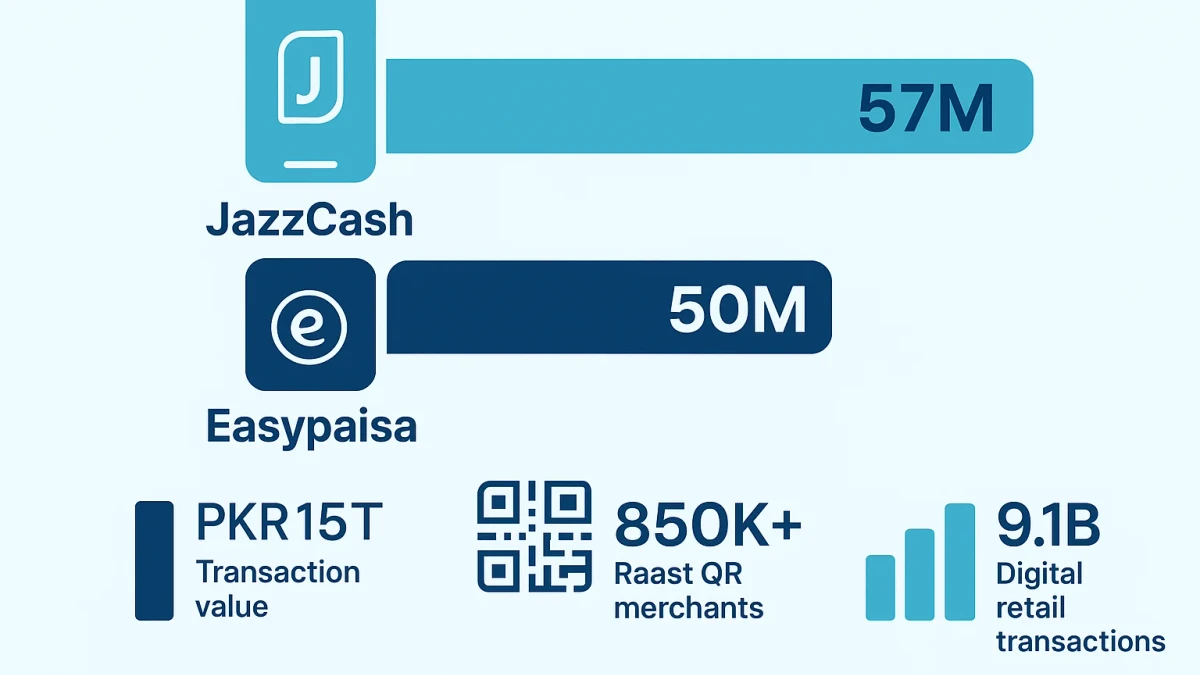

The infrastructure question was settled in 2024-2025. JazzCash crossed 57 million customers in December 2025, processing PKR 15 trillion in gross transaction value. Its Raast-enabled QR merchant network exceeds 850,000 outlets across Pakistan. Easypaisa maintains 50 million registered users, processing 2.1-2.8 billion annual transactions worth PKR 7-9.7 trillion. Combined, these two wallets cover the majority of Pakistan’s adult population with smartphone access.

The State Bank of Pakistan’s Raast instant payment system processed 9.1 billion digital retail transactions in FY25, creating a settlement layer that makes person-to-merchant payments nearly instantaneous and virtually free. According to FundinFolks’ Pakistan fintech analysis, 84-88% of retail transactions now flow through digital channels. The rails exist; the missing piece is ecommerce checkout design that makes the digital path feel as safe as handing cash to a rider.

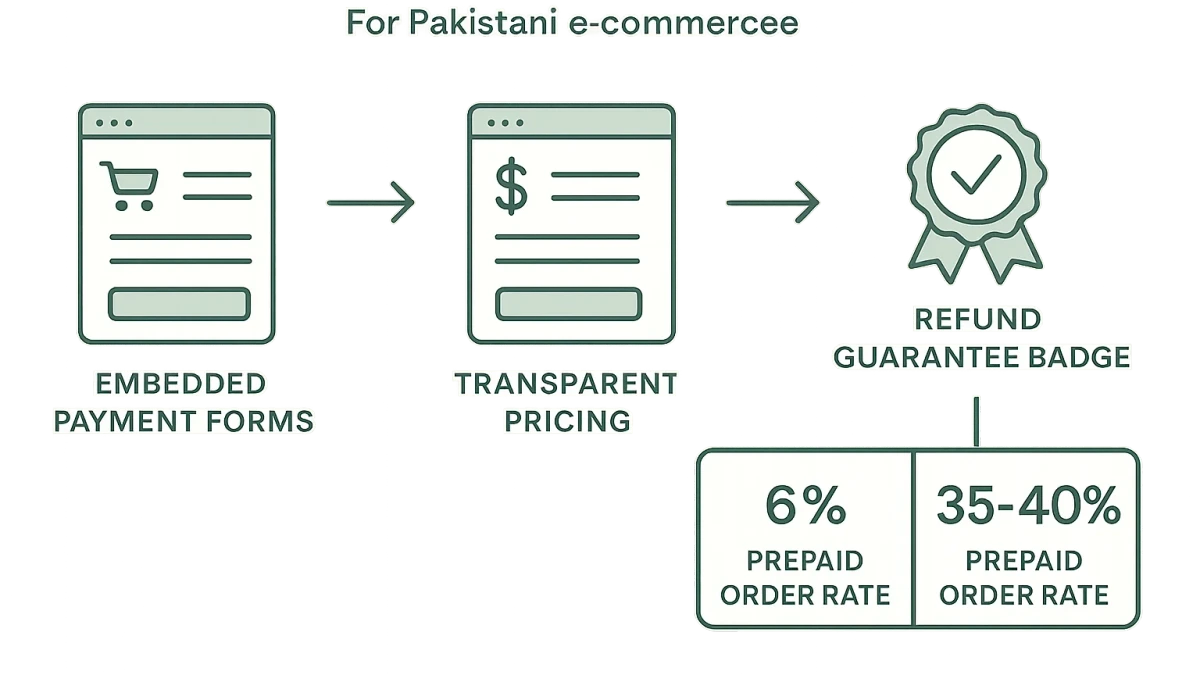

WeProms Digital, Pakistan’s leading ecommerce conversion optimization agency, has found that stores implementing wallet-first checkout with JazzCash and Easypaisa see prepaid order rates jump from 6% to 35-40% within 60 days. Not by removing COD as an option, but by making the prepaid path the visually and functionally primary choice at checkout.

What breaks at checkout that sends buyers back to COD?

Three specific design failures push buyers toward COD on Pakistani stores. First, payment gateway pages redirect users away from the store to a third-party interface — often a bank page with poor mobile rendering and no Urdu language support. The buyer sees an unfamiliar URL, a loading spinner, and hits the back button. Second, the price displayed at checkout changes when processing fees appear; a PKR 3,500 order suddenly shows PKR 3,588 with “convenience fee” text that signals anything but convenience. Third, there is no explicit refund policy visible at the payment step, leaving the buyer wondering what happens if the product arrives damaged after they have already paid.

Each of these failures is solvable. Embedded payment forms that keep the user on-domain, transparent pricing that folds gateway fees into the product margin, and a one-line refund guarantee next to the payment button — “Full refund within 48 hours if the product doesn’t match” — address the three primary trust gaps. Dawn’s analysis of Pakistan’s mobile wallet landscape notes that JazzCash maintains 21 million monthly active users while Easypaisa holds 18 million; these users are already comfortable transacting digitally. The checkout experience simply needs to match the trust level they already have with their wallet app.

Pakistani ecommerce platforms that implemented JazzCash and Easypaisa direct integration — not redirect-based gateways — reported a 25-35% increase in prepaid orders within the first month, because the checkout flow mirrors the wallet experience the user already trusts.

What happens when Pakistani stores flip the default payment method?

When a Peshawar electronics store changed its checkout default from “Cash on Delivery” to “Pay with JazzCash” — without removing COD as an option — prepaid orders increased from 8% to 31% in three weeks. The store did not offer a discount for prepaid. It did not run a campaign. The only change was visual hierarchy: the JazzCash button appeared larger, above the fold, with a “Recommended” badge, while the COD option sat below in smaller text.

This is not an isolated case. According to PakAccountant’s digital payments tracking, digital payments surged 84% in 2024, reaching 6.4 billion transactions worth PKR 547 trillion. The growth came not from new technology but from better integration — apps making the digital path one tap shorter than the cash alternative. DMT Lahore’s Pakistan ecommerce analysis projects the ecommerce market reaching PKR 500 billion by 2026, with 35% of online retail flowing through social commerce channels where digital payment is the default.

The principle is straightforward: Pakistani consumers choose the path of least cognitive resistance. When COD requires fewer decisions than digital payment, COD wins. When digital payment is presented as the default with familiar wallet logos and one-tap confirmation, digital payment wins. The technology has been ready since 2024. The checkout design has not caught up.

For Pakistani ecommerce stores, the decision criterion is this: if your prepaid order rate sits below 20%, your checkout is actively losing money — not because Pakistan refuses to pay digitally, but because your store has not built the trust architecture to make digital payment feel as safe as cash. At WeProms Digital, Pakistan’s leading ecommerce marketing agency, we build complete checkout optimization systems that integrate JazzCash, Easypaisa, and Raast directly into the purchase flow, reducing returns by 60-70% and cutting customer acquisition costs by up to 25%. If your Pakistani store is losing margin to COD returns and delayed remittances, reach out via WhatsApp or email hello@weproms.com.

Frequently Asked Questions

How we helped a Pakistani business achieve measurable results.

How do I add JazzCash and Easypaisa to my Pakistani ecommerce store without a payment gateway?

Both JazzCash and Easypaisa offer direct merchant integration APIs that bypass traditional payment gateways. JazzCash provides checkout buttons through its Business Portal, and Easypaisa offers a Merchant Account with QR and link-based payments. These integrations keep the user on your domain and avoid redirect-based trust erosion.

Will removing COD as an option hurt my Pakistani ecommerce sales?

Removing COD entirely can reduce order volume by 20-40% in the short term. Instead, make digital payment the visual default — larger button, above the fold — while keeping COD available. Pakistani stores using this approach see prepaid rates rise to 30-40% without losing overall orders.

What is the typical return rate difference between COD and prepaid orders in Pakistan?

COD orders in Pakistani ecommerce carry a 30-40% return-to-origin rate, while prepaid orders return at 5-8%. Customers who have already paid are more deliberate about their purchase decision and significantly less likely to refuse delivery.

How does Raast integration help Pakistani ecommerce stores?

Raast enables instant, low-cost person-to-merchant payments through QR codes and mobile wallet integration. For ecommerce stores, Raast settlement is near-instantaneous compared to the 7-14 day COD remittance cycle, improving cash flow and eliminating courier collection fees of 2-3%.

Sources & References

- BeingGuru — Pakistan E-commerce Surpasses $10.4B: ADB Report Reveals — 2025

- TechJuice — Easypaisa vs JazzCash: The Ultimate Mobile Wallet Showdown — 2025

- FundinFolks — Pakistan Fintech Market Analysis — 2025

- ATNRCO — Ecommerce Marketing in Pakistan — 2025

- PakAccountant — Digital Payments Growth in Pakistan — 2024

- Dawn — JazzCash vs Easypaisa Mobile Wallet Users — August 2025

- PACRA Research — Pakistan Media Sector Report — February 2025

Additional reading from industry feeds: